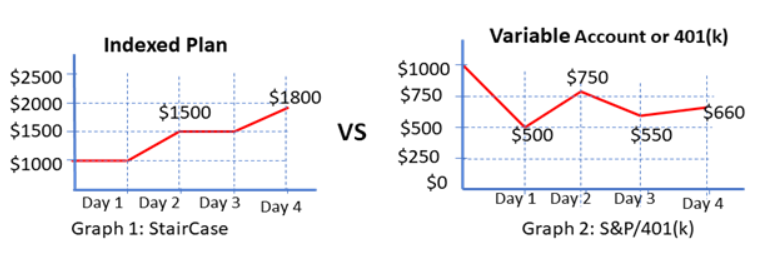

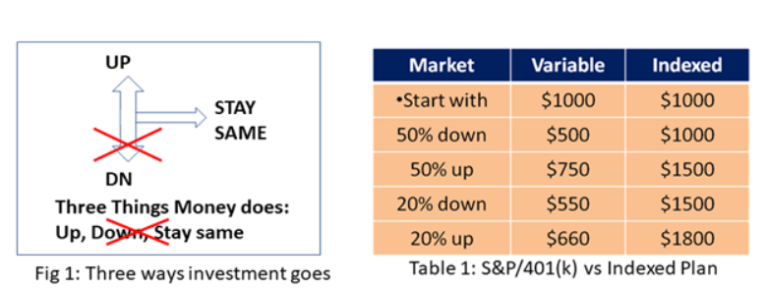

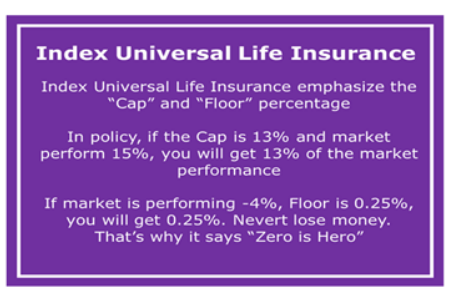

Indexed Universal Life insurance policy emphasizes the cap and floor rate. Therefore the returns are guaranteed because of the floor rate the policy offers. This further means that even if the index is in loss, your account will be credited. The policyholder will not lose any money or be negatively impacted in any given situation. For example: You policy has cap rate of 13% and market performs 15%, you will get 13% of the market performance. If market performs -4%, floor is 0%, you will not lose money. This is why it calls “Zero is Hero.” Over the last 20 years, market has performed close to 80%

Medical Insurance

Our life is unpredictable. No one knows what will happen at any age. Spending too many hours at work is a leading cause of burnout, heart attack and stroke. What if you had a heart attack and treated at the hospital. Health insurance pays 50 to 80%, rest 20 to 50% comes from your savings. What if insurance pays the 20 to 50% would you call it an investment? Yes, I will. This insurance policy covers heart attack, stocks, cancer, heart disease, lung disease, liver disease, and more at no extra cost. Moreover, this policy gives you tax-free retirement for life with other benefits.

Life and health fragile and no one know what will happen tomorrow. You don’t have to buy Terminal Illness, Critical Illness, and Chronic Illness coverage because it comes with a policy.

Tax-Free Retirement

IUL offers a great retirement plan as long as you continue to make payments on the policy, the cash value will grow tax-deferred. If you start early, by the age of 65 you will have good tax-free retirement for life. Upon your death, your family will get the tax-free death benefit.

However, if you withdraw money from the policy before age 59 ½ you may have to pay tax on gain. Please note that if the loan is not paid back, your death benefit will be used to balance the loan due. This is where you have to be careful about it

No Limit on Premium Paid

Another reason why IUL/Tax-Free retirement plan is the best option and most preferred is that IRS has established no limit with premiums paid with indexed universal life insurance into LIRP (life insurance retirement plans). However, options like Life Insurance Retirement Plans such as 401k or IRA have limitations.

For example, in a 401(k) plan, the annual contributions are limited to approximately $20,500 annually. This can seriously impact your wealth accumulation when you reach the mandatory distribution age of 70 ½.

Death Benefit

IUL is insurance with death benefit plus it has living retirement benefit. This makes the policy benefit in both ways. If you, the policyholder, die early, your beneficiary will be given a tax-free death benefit, thereby it becomes easier for them to pay for your funeral expenses without the financial burden. On the other hand, if you live long, you can enjoy the savings after retiring and continue to maintain your lifestyle.

No Penalty on Withdrawal

Physicians, Dentists, and DVM’s can take money out from saving for their business without penalty at any age. If you have a 401(k) policy and wish to withdraw money before 59 ½ years of age, you will have to pay income tax on the withdrawal amount. In the majority of cases, this is around 10 percent. However, with IUL, you can withdraw money at any time without any tax liability or penalties.

Family Protection

This policy is a very powerful financial tool for protecting the financial well-being of your family for decades to come—even after death. With this policy in hand, you will have the flexibility to build assets and deal with life's uncertainties. Ever since 2020, many medical professionals, including physicians and nurses, have lost their lives in the quest of saving others from COVID-19. They are our real heroes.

Nonetheless, those medical professionals at the forefront, putting their lives at risk in saving the lives of patients from COVID-19; they need their own and family protection if something happens to them. You can borrow against the savings in policy for your children’s education, down house payment, or buy a car. Medical coverage can be used for any uncertainties that may come in future.

Loan Availability

Withdrawals will reduce your cash-value dollar to dollar. Full Surrender may have some tax implications. With IUL, you get the flexibility of taking out a loan without facing penalties, credit checks, or taxes. It will not reduce your cash-value account. Moreover, you don't have to return the money you take out. This makes the policy far more attractive than other options available.