We are licensed with one priority—you and your family. Therefore, our team is strongly committed to helping you find the best annuity, life and health insurance coverage policies customized to fit your needs, goals, and budget so that you and your family can experience and enjoy the best things in life worry-free!

Here is a quick overview of SGLI (Servicemembers’ Group Life Insurance), Veteran Group Life Insurance (VGLI), and Indexed Universal Life Insurance (IUL):

When I joined the Armed Forces, I automatically signed up for Servicemembers’ Group Life Insurance. SGLI is a low-cost term life insurance providing maximum coverage of $400,000. It is accessible by members of the uniformed services. SGLI is purchased by the Department of Veterans Affairs, where servicemembers are insured automatically unless they decline the coverage.

Upon release of service, SGLI members have two options. They can either convert their full-time SGLI coverage to renewable term insurance under the VGLI program or opt for a temp/permanent life insurance plan with a private insurance company.

The VGLI plan is a continuation of the SGLI plan. It is available to servicemembers’ who are retiring or separating from the military. If you convert your SGLI to VGLI within 240 days there is medical exam or medical questions. However, after 240 days to 1 year and 120 days, you will have to complete an application with all the compulsory health questions. Hence, the application approval will be based on your health condition. Moreover, after 1 year and 120 days, you will no longer be eligible to convert your SGLI plan to VGLI. Therefore, it is advisable to keep the timelines in consideration and apply promptly for private life insurance.

Please note, VGLI is a term life insurance policy. It wouldn’t give you retirement because it doesn’t have cash saving account in the plan. Furthermore, the premium increases every five years. Let’s suppose you buy a $400,000 death benefit VGLI:

Many people believe Death Benefit is the main purpose of life insurance but they don’t know life insurance has evolved to become a financial saving, retirement, investment, education saving and tax optimization tool including keeping primary purpose is to provide a death benefit.

Even you have SGLI or VGLI, it’s always good to sign-up for the private life insurance policy – Index Universal Life Insurance for following reasons:

My grandson is signed up for Index Universal Life Insurance. At age 65 this kid will receive $579,000/year for tax-free retirement. Total premium pad in 60 years: $349,000 and by age received $14.47 million.

Indexed Plan is Tax-Free Retirement and permanent life insurance which comes with a tax-free retirement plan, life insurance and medical insurance such as critical illness, chronic illness and terminal illness. Some investors referred to this as one of the best tax-free retirement and medical products. The premiums are determined on the basis of policy type, face amount, age, risk evaluation based on health status and optional riders. Premium covers the cost of insurance and expenses and the remaining premium goes to a cash-value account where it grows via fixed and indexed account, such as the S&P 500 or the Nasdaq-100. Cash-value accumulation occurs within two sub-accounts: Fixed account and Indexed account.

The main purpose of using this policy is to accumulate wealth through a tax-deferred interest crediting basis. The excess premium paid by the policyholder is placed in the sub-account that continues to earn interest on an index like S&P 500 or NASDAQ. IUL is an attractive option because it is not as volatile as other policies available in the market. This is because your money is not invested in the equities in real, but the insurance company mimics the index returns.

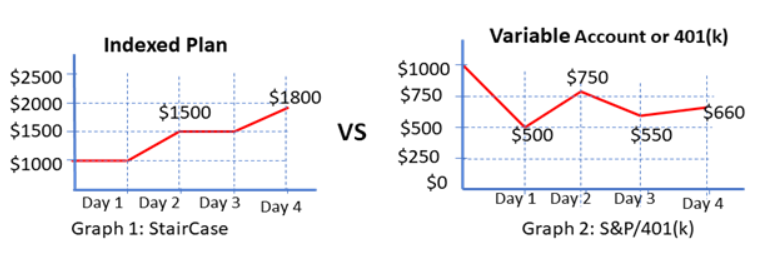

Graph 1 shows investment in IUL (Indexed). It’s like a staircase. Money always goes up or stays the same. Your savings never go down as shown in Graph 2. It earns compound interest on indexed based formulas. Your investment is earning money rather than losing.

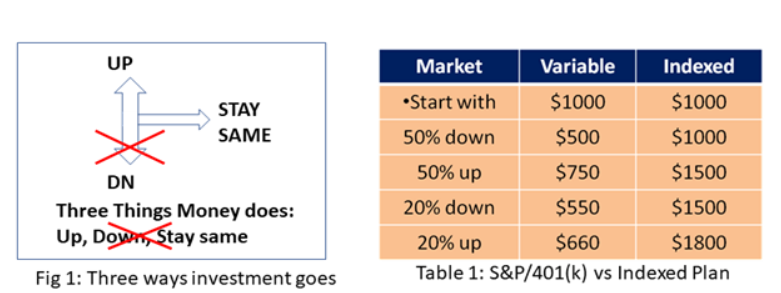

So what is an Indexed account? Fig 1 shows money goes three ways. Goes up, stays the same or goes down. In an indexed account money goes up or stays the same but never goes down. Your money is protected from going down. It is a guarantee that you will never lose money.

Graph 1 shows StairCase and Table 1 shows Variable Account (401(k) vs Indexed plan. When the market is 50% down, saving in an Indexed plan stays the same at $1000. When the market goes 50% up, indexed accounts accumulate 50% interest. So the Indexed account will have $1,000 + $500 = $1,500 in savings.

Graph 2 shows a variable chart and Table 6 shows a variable account. When the market is 50% down, saving in 401(k) loses $500. When the market goes 50% up, saving in 401(k) earns $250. This comes out to be $500 + $250 = $750 in 401(k) savings.

Now we know how the market plays a big role in our investments.

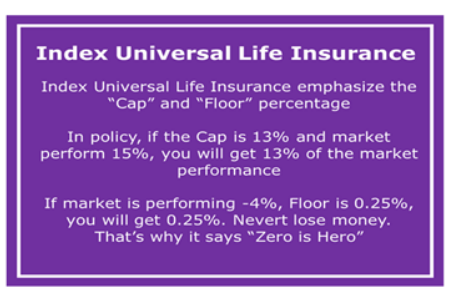

Indexed Universal Life insurance policy emphasizes the cap and floor rate. Therefore the returns are guaranteed because of the floor rate the policy offers. This further means that even if the index is in loss, your account will be credited. The policyholder will not lose any money or be negatively impacted in any given situation. For example: You policy has cap rate of 13% and market performs 15%, you will get 13% of the market performance. If market performs -4%, floor is 0%, you will not lose money. This is why it calls “Zero is Hero.” Over the last 20 years, market has performed close to 80%

Our life is unpredictable. No one knows what will happen at any age. Spending too many hours at work is a leading cause of burnout, heart attack and stroke. What if you had a heart attack and treated at the hospital. Health insurance pays 50 to 80%, rest 20 to 50% comes from your savings. What if insurance pays the 20 to 50% would you call it an investment? Yes, I will. This insurance policy covers heart attack, stocks, cancer, heart disease, lung disease, liver disease, and more at no extra cost. Moreover, this policy gives you tax-free retirement for life with other benefits.

Life and health fragile and no one know what will happen tomorrow. You don’t have to buy Terminal Illness, Critical Illness, and Chronic Illness coverage because it comes with a policy.

IUL offers a great retirement plan as long as you continue to make payments on the policy, the cash value will grow tax-deferred. If you start early, by the age of 65 you will have good tax-free retirement for life. Upon your death, your family will get the tax-free death benefit.

However, if you withdraw money from the policy before age 59 ½ you may have to pay tax on gain. Please note that if the loan is not paid back, your death benefit will be used to balance the loan due. This is where you have to be careful about it

Another reason why IUL/Tax-Free retirement plan is the best option and most preferred is that IRS has established no limit with premiums paid with indexed universal life insurance into LIRP (life insurance retirement plans). However, options like Life Insurance Retirement Plans such as 401k or IRA have limitations.

For example, in a 401(k) plan, the annual contributions are limited to approximately $20,500 annually. This can seriously impact your wealth accumulation when you reach the mandatory distribution age of 70 ½.

IUL is insurance with death benefit plus it has living retirement benefit. This makes the policy benefit in both ways. If you, the policyholder, die early, your beneficiary will be given a tax-free death benefit, thereby it becomes easier for them to pay for your funeral expenses without the financial burden. On the other hand, if you live long, you can enjoy the savings after retiring and continue to maintain your lifestyle.

Physicians, Dentists, and DVM’s can take money out from saving for their business without penalty at any age. If you have a 401(k) policy and wish to withdraw money before 59 ½ years of age, you will have to pay income tax on the withdrawal amount. In the majority of cases, this is around 10 percent. However, with IUL, you can withdraw money at any time without any tax liability or penalties.

This policy is a very powerful financial tool for protecting the financial well-being of your family for decades to come—even after death. With this policy in hand, you will have the flexibility to build assets and deal with life's uncertainties. Ever since 2020, many medical professionals, including physicians and nurses, have lost their lives in the quest of saving others from COVID-19. They are our real heroes.

Nonetheless, those medical professionals at the forefront, putting their lives at risk in saving the lives of patients from COVID-19; they need their own and family protection if something happens to them. You can borrow against the savings in policy for your children’s education, down house payment, or buy a car. Medical coverage can be used for any uncertainties that may come in future.

Withdrawals will reduce your cash-value dollar to dollar. Full Surrender may have some tax implications. With IUL, you get the flexibility of taking out a loan without facing penalties, credit checks, or taxes. It will not reduce your cash-value account. Moreover, you don't have to return the money you take out. This makes the policy far more attractive than other options available.

1. Flexible premium, skip premium

2. Option to pay a minimum premium to keep policy in force

3. Option to pay maximum within federally established tax lay

4. Tax free retirement

5. No plenty and age limit on early withdrawal

6. Take loan against the cash value while cash value is earning interest

7. Saving never run out as long as you live

8. Death benefit – Family protection

9. Fast cash accumulation, Cash Value – Saving account

10. Risk free – Never loses money even the market crash. In 2008, 401k lost money but IUL didn’t

11. Loan option to buy house, car, medical bills

12. Tax free education plan

13. Full access to saving account

14. Not considered an asset when calculating the amount for financial aid

15. Use money at any College & University

| VGLI | IUL | |

| Insurance Policy Type? | Term insurance policy | Permanent Life insurance |

| Any retirement plan? | No | Yes, Risk free retirement saving plan |

| Policy Premium rate | Yes, Premium rate based on your age and policy value. Every 5 years the rate goes up. Gets very expensive after age 60.

For $400K death benefit: At age 64 -69 premium $588/month At age 70-84 premium $904/month At age 75-79 premium $1712/month |

Yes, IUL Premium rate is based on your age, coverage, and health. Fixed premium. Never change |

| At age 64 & above some of you may not need insurance but need more money | VGLI is expensive. You may cancel it!!! | IUL will provide you Retirement with Terminal illness, Chronic illness, & Critical illness policy |

| Premium Recovery | No Recovery | Get your money back within 6 years |

| Is there a Death Benefit? | Yes, Policy Face Value | Yes, Policy Face Value and increase |

| Is there any education saving | No | Education saving benefits – cash-value account |

| Is there a loan option? | No | There is no age limit when you withdraw or take out a loan from your savings plan. Pay no income tax on cash accumulation over the years |

| Is there rider option | No | Add several riders for financial protection under unexpected circumstances |

| Is there any contribution limits? | NA | No limit on contribution to increase cash-value account |

| Fixed or Level premium? | Change every Five year based on age | Policy premium is fixed and flexible. Never change. |

| Are premium rates increased for smokers? | No. Premium rates are the same for smokers and non smokers | Yes and No. It’s depend when your stop smoking. Premium rate is based on health questions. |

| Will I need to answer questions about my health? | You have to apply within 1 year and 120 days for VGLI.

No, If you apply within 240 days there will be no health questions. Yes, If you apply after 240 days there will be health questions. |

Yes, there are health questions. Policy approval rate may be a little higher if you are a smoker. For more information, please ask a Licensed Financial Advisor/ Insurance agent. |

| Are premium rates based on age? | Yes, Insurance policy premium rates are based on your age and the face value/death benefit. view VGLI premium rates |

Yes, Insurance policy premium rates are based on your age and the face value/death benefit. |

| Are premiums rates different for men and women | No, Premium rates are the same regardless of gender. | Yes, but there is not much difference. |

| Will anyone help me in figuring out the right amount of insurance coverage? | Yes - VGLI has an objective Insurance Needs Calculator to help you determine how much coverage you need. | Yes, Licensed Financial Advisor/Insurance agent will help you |

| When is my insurance coverage effective? | Your full insurance coverage amount is effective as soon as you are approved and your premium is paid. | Your full insurance coverage amount is effective as soon as you are approved and your premium is paid. |

| Will my insurance coverage end at a specific age or after a period? | No, Policy coverage will not end unless you request it or fail to pay premiums. | No- Your IUL coverage will not end as long as you pay the premium. |

| Can I be excluded from coverage due to vocation or avocation? | No, The policy does not exclude applicants based on their job or recreational activities. | No- there will be no change to the coverage and policy |

| Can I choose how often to pay the premiums? | Yes – You can choose your premiums: monthly, quarterly, semiannually or annually. | Yes – you can choose to pay your premiums: monthly, quarterly, semiannually or annually |

| Are there special benefits for the terminally ill? | Yes - You can request a payment of up to 50% of your VGLI coverage if you are diagnosed with an illness that results in a life expectancy of 9 months or less. | Yes, Automatelicly at no cost, the policy provides three free riders: Terminal Illness, Critical Illness, and Chronic Illness |

| Is there a contestable period? | No - VGLI has no contestable period. That means there is no waiting period between when your coverage begins and when a claim would be paid. | No waiting period. It’s active once you pay a premium and approve. |

| Can I manage my insurance coverage | Yes – VGLI has a full service web site. | Yes, every year you can ask your insurance company for Illustration and full service website available to you |

IMPORTANT TO KNOW:

After using money for college education, continue paying premium, Your Child would have:

(1) Tax-Free Retirement Plan for your Child

(2) No need to buy family protection for his family.

(3) If in some case bad happened with health, you child will be covered under critical illness, chronic illness and terminal illness

(4) Take money out for house down payment or buy new car or buy business

(5) Premium will never go up like other life insurance companies.

It's always wise to have a life insurance policy for your children and grandchildren. This is not the reason that they die before you and you collect the money. It creates (1) College saving (2) Tax-free retirement. (3) Family protection and (4) Medical Benefits, such as chronic illness, Critical Illness, and Terminal Illness.

CLICK HERE FOR VIDEO IN ENGLISH COLLEGE SAVING PLAN

CLICK HERE FOR VIDEO IN SPANISH COLLEGE SAVING PLAN

CLICK HERE FOR VIDEO IN ENGLISH EXAMPLE: 26 YEAR OLD MALE RETIREMENT PLAN

CLICK HERE FOR VIDEO IN SPANISH EXAMPLE: 26 YEAR OLD MALE RETIREMENT PLAN

CLICK HERE FOR VIDEO IN ENGLISH EXAMPLE: 42 YEAR OLD MALE RETIREMENT PLAN

© 2022 American Financial Consulting. All rights reserved.